Increasing Access to Microcredit to Encourage Business Start-up and Participant Welfare in Bosnia and Herzegovina

- Adults

- Earnings and income

- Enrollment and attendance

- Self-employment

- Business investment

- Credit

Microcredit is widely believed to create opportunities for entrepreneurs and families to improve their economic and social well-being. Researchers expanded microcredit offerings in Bosnia and Herzegovina to evaluate the effect of improved credit access on economic and social outcomes. They found that providing loans to slightly under-qualified microcredit applicants increased small business ownership, but not income, and decreased school participation among high school-aged youth who worked more in family businesses.

Problema de política pública

The rapid growth of microfinance institutions (MFIs) has brought formal credit to millions of low-income households around the world, yet there is still much debate about whether microcredit reduces poverty. Many MFIs have moved from the group loan model of microcredit, pioneered by the Grameen Bank in the 1970s, to an individual loan model that requires applicants to provide collateral. Collateral and other eligibility requirements may prevent some low-income individuals with potentially profitable investments from qualifying for microloans. Yet, there is little rigorous evidence about whether providing microloans to slightly more risky clients by lowering collateral requirements can improve the clients’ well-being, or whether it is profitable for MFIs. How do microloans affect the small business investments, incomes, and labor decisions of poorer households who have traditionally been excluded from microcredit?

Contexto de la evaluación

Bosnia and Herzegovina has an active microcredit market, but poorer segments of the population have typically not been served by MFIs. Prior to this study, the microfinance applicants who participated earned an average annual income of about US$11,100. On average, around 40 percent of their annual income came from self-employment. Nearly one third of the applicants had only completed primary school, while 5 percent had attended university. The study took place at the height of the global financial crisis of 2008 and 2009, which strongly affected Bosnia and Herzegovina. During the study, many MFIs experienced dramatic increases in late and non-repayment.

Detalles de la intervención

In partnership with a major Bosnian MFI, researchers conducted a randomized evaluation to examine the impact of microcredit on business investment, income, and household consumption and savings among Bosnian microcredit applicants who were slightly under-qualified for the MFI’s traditional loans. To find marginal microcredit applicants, the MFI’s loan officers were trained to identify a portfolio of clients who they would normally reject, but to whom they would consider lending to if the MFI allowed loan officers to accept slightly more risk.

Once a loan officer identified a potential marginal client, and following a short vetting process from a loan committee at the MFI, they would explain the aim of the study to the client. On condition of participating in the baseline survey and a follow-up survey fourteen months later, the clients were offered a 50 percent chance of receiving a loan. In total 1,196marginal loan applicants were approved and interviewed in the baseline survey. Researchers then randomly assigned the applicants to either receive a microloan, or serve as part of the comparison group. Six hundred thirty-seven applicants were randomly chosen to receive a loan and the remaining 569 applicants served as a comparison group. The average loan size was just over US$1,000. Borrowers were required to make monthly repayments and the annual interest rate was 22 percent, which was one percentage point higher than interest rates given to the MFI’s regular clients.

Resultados y lecciones de la política pública

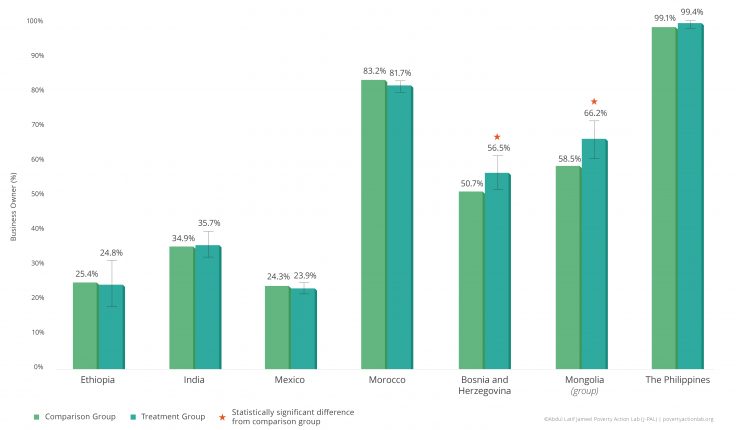

Business activities: The microloans led to increased business ownership and self-employment, but did not increase business profits or income within the fourteen month study period. Households who received microloans were 6 percentage points more likely to own a business than households in the comparison group, but increased business ownership and self-employment did not lead to increased income relative to comparison households.

Consumption: After receiving a loan, households with less education significantly reduced their weekly food consumption at home by 15 percent (around US$13). Households with savings, who tended to be households with more education or those who already owned a business, instead significantly reduced their savings in order to finance investments This suggests that households still had to find additional resources beyond the microloan to be able to make the desired investments in their businesses, and that those without savings did so by reducing their food consumption.

School participation and youth labor: Microloans led to decreased school participation among young adults aged 16 to 19 in lower education households, and increased the probability that young adults aged 16 to 19, in general, were employed within their families’ small businesses. Young adult children of microloan recipients worked around half an hour more per household each week than young adults from households in the comparison group.

As they began to work more in their family businesses, there was also some evidence that school participation among 16 to 19 year olds in the treatment group decreased. Overall, children aged in this age group were 9 percentage points less likely to attend school after their household received a microloan, and 19 percentage points less likely if they came from a household headed by someone with only a primary school education.

Commercial viability of the program: Lending to slightly riskier clients was not profitable for the MFI due to a high level of late and non-repayments among households that received a loan. Ultimately, the MFI lost approximately US$268 per US$1000 loan it issued to the marginal microcredit applicants. Researchers therefore concluded that lowering collateral requirements to lend to slightly under-qualified borrowers was not commercially viable, at least in the period of financial crisis in which the study took place.