Image

Contrary to popular beliefs, welfare programs are often under-subscribed. A recent review of program take-up in OECD countries estimates that only 40–80 percent of eligible individuals and households actually apply to social assistance and housing programs. There is limited data on the take-up in developing countries, but we know that coverage of these programs is low. According to the World Bank’s Atlas of Social Protection Indicators of Resilience and Equity database, only 22 percent of the poorest households in sub-Saharan Africa receive any form of social assistance. Further, we know for some specific programs this low coverage is driven by low take-up. For example, in India the take-up of an unconditional cash transfer for poor widows and divorcees in Delhi is particularly low—many eligible women simply do not take up the program.

One of the reasons for the low take-up of welfare programs is the lack of access to legal IDs, which are typically required to access the program. Close to 40 percent of adults in low-income countries do not have an ID. Women and vulnerable groups are disproportionately less likely to have an ID.

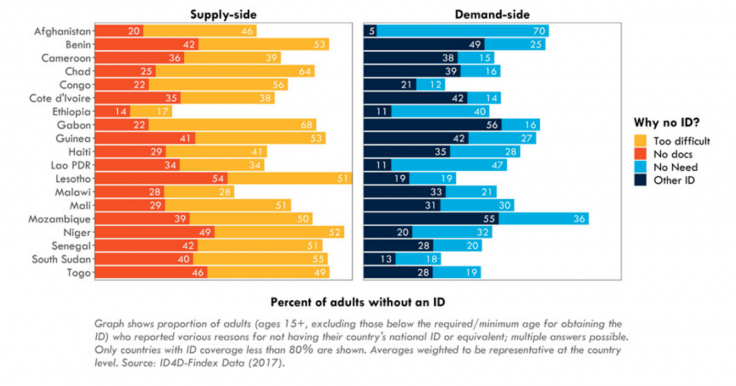

Although many people who do not have an ID cite reasons related to difficulties during registration, such as distance to the registration center, the take-up of IDs is also closely related to the perceived benefits of having an ID, along with the substitutability of the ID with other forms of identification. If an individual is able to use their driver's license interchangeably with their national ID, beneficiaries may not see the use of registering for an ID. As of 2017, 40 percent of adults without an ID in Ethiopia responded that they do not have the ID because they have no need for one. In Mozambique, 36 percent of adults without an ID reported a similar reason.

In addition to the (perceived) lack of IDs, there are other possible barriers to the take up of welfare programs:

Mass rollout of digital IDs and digital payment systems offer a possible solution. A coordinated effort, with an associated information campaign, can be effective in overcoming some of the barriers to take up and in increasing coverage of welfare programs. Many countries have already started implementing nationwide ID systems for this very reason. For example, between May and December 2017 approximately 9.1 million Malawi citizens were registered with their biometric attributes and obtained a digital ID. The Malawi National Registration Bureau achieved the target for near-universal coverage. Although Malawi is seen as a success, Figure 1 shows the more systematic problem of lack of ID coverage. Digital payment systems could also allow direct benefit transfers to beneficiaries and better targeting, reducing many of the barriers to accessing welfare benefits.

Digitization reduces administrative barriers. The ability to link beneficiary data across departments allows for a potentially less bureaucratic process with fewer forms and less redundancy. In addition, digitization, such as access to a digital ID, allows for registration online or remotely with fewer in-person requirements. The remote nature could have a large effect on the ease of operations from a beneficiary perspective and also increase their willingness to engage with the platform. For example, governments could consider mobile money payment options for subscribers to process their annual renewal fees. This shift to digital payments would reduce transaction costs for both the government and beneficiaries by eliminating the need to appear in person to complete this task.

For example, the Togolese government, in response to the COVID-19 pandemic, implemented the Novissi digital transfer program for informal workers. Individuals could apply for the transfer using their mobile device and also received their disbursements through mobile money. The digital system allowed for a smooth, safe implementation with less need for in-person disbursement and more transparent transfers of funds. Further, this program used the voter ID database from the February 2020 presidential elections, which contained precise location and occupation information, to identify beneficiaries. Hence, beneficiaries did not need to jump through several administrative hoops to prove their eligibility because of the government’s ability to use pre-existing data.

A more digitized and streamlined process could also allow for reductions in processing time for individuals registering for the digital ID or payment platform. There is some initial evidence from India, which suggested that the digitization assisted with improving implementation efficiencies and in decreasing the time spent in line waiting to receive the program benefits.

A review of literature regarding the take up of social programs in the United States and United Kingdom highlights that lack of information, in addition to complicated eligibility requirements, can limit the collection of social protection payments. Technology has the potential to improve these information flows between government and citizens.

Mobile technologies provide a channel through which to easily send reminders to beneficiaries, especially for programs with multiple steps for enrollment. ID enrolment, for example, is often a two-step process—first users register, then they collect their physical card. Mobile technologies can be leveraged to remind individuals to collect the digital ID card once the card has been printed. This reminder could assist with overcoming potential behavioral biases and nudge individuals to complete enrollment processes. For example, a Digital Identification and Finance Initiative (DigiFI) funded study plans to explore whether mobile pension payment coupled with the inclusion of a national digital identification card and voice messages, explaining the importance of pensions, can nudge pension contributions in Ghana.

It is worth noting that while information delivered via mobile technology can assist with take-up for those who are literate, it will not assist the most vulnerable who are unable to read (as evidenced by a study in India). However, information plus enrollment assistance was more effective in increasing application rates and encouraged more vulnerable women (e.g. those who were illiterate, politically disadvantaged, and who lacked autonomy in their households) to apply. Some social programs may remain complex and require additional thinking regarding the registration process. Digital registration alone is not always the most constructive pathway.

Effective implementation of government systems is important on many levels, including in ensuring citizen trust in the state, which may impact their likelihood of taking up government welfare programs. Information interventions that leverage technology to improve engagement with the program—such as providing information through technology platforms that currently exist—may be able to bolster trust and hence take-up of programs.

However, the malfunctioning of technology could backfire and reduce trust in institutions leading to adverse outcomes. Researchers found that the text message campaign led to a small increase in voter turnout but significantly decreased trust in the functioning of the electoral commission, especially among voters linked to the party that lost the election for president.

DigiFI is interested in a number of open questions on the registration and use of digital IDs and payment systems to improve the coverage and take-up of welfare schemes. Specifically, we are interested to learn more about how policymakers and NGOs can use data generated through digital ID and payment schemes to reduce administrative barriers and decrease transaction costs, with the goal of ultimately improving the take-up of underutilized programs? To learn more, read the DigiFI framing paper for information on our research agenda and other open questions.

Authors Note: This is the seventh blog in the DigiFI series on the various aspects of their research and policy priorities. The next blog will focus on high-frequency process monitoring systems that leverage digitally collected data.